Everyone doesn't hate them. The HN and reddit crowds are relatively small. The "general population" still loves to play Candy Crush every chance they get.

One could say it's an opportune time for them. New investors are more than just bag holders. They become promoters who are sympathetic to King's crusade.

Well ... since that's likely to be their only enduring IP (most of their game concepts seem copied), perhaps they need to play up the fact that they've trademarked the word "Candy" to pump the valuation of their IPO.

Sounds like 3rd party Candy Crush revenue estimates, which have consistently hovered around $700K/day, were way off. The filing says Candy Crush is responsible for 78% of revenue - that's $1.48 billion in 2013. That's more like $4 million/day.

Makes me wonder how far off third party estimates for other apps are.

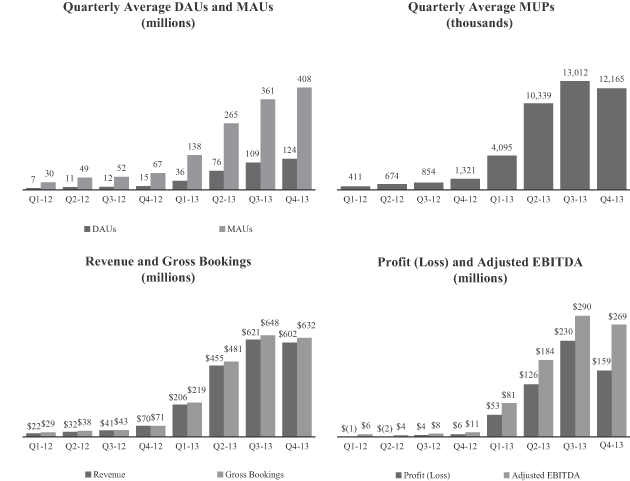

It shows that the monthly unique payers (MUPs), revenue and profits were all lower in Q4'13 than they were in Q3'13. Investors will want to know whether Q3'13 was the peak (and it's all downhill from here) or whether Q4'13 was a blip and Q1'14 resumes the upward trend.

Smart investors are wary of one-hit wonders. I heard that Rovio's March 2011 investment round was based on a valuation of 1x revenues. Mind Candy is working on three new franchises that it hopes will replace Moshi Monsters, which has seen traffic from the UK and US drop by ~50% over the past year.

Zynga's share price was priced at $10 when it IPO'd in December 2011. It peaked at $14.69 in March 2012 and is trading at less than $5 today.

If King's Q1'14 numbers are lower than Q4'13, I would not expect the IPO to go ahead. Companies in this space need to demonstrate the ability to repeat the success of hits like FarmVille, Angry Birds, Candy Crush and Moshi Monsters.

I don't think I'm ready to touch social gaming stock with a 10 foot pole. It'll probably have a nice bump right after the stock goes public, but I sense a large crash in its future. The social gaming market is just so fickle.

I'm not so sure. The puzzle matching games are easier to grasp than Zynga's ville-type games. I'm trying to say that games from King have a lower common denominator.

They definitely do, yet since Zynga was on top of Facebook, seeing friends play the game and shoving shit in their face made people play as well. I actually forgot that we're talking about mobile applications here. Not sure if Candy Crush and stuff is directly on Facebook...maybe they will be more successful than Zynga.

Their numbers imply that not only is Candy Crush much bigger than their other games, it is more effective per-user in engagement and revenue as well. So they run a real risk (which they acknowledge in the filing) that dilution of their player base with more games in the same genres may actually hurt their business. However, cross-promoting games in different genres will be much less effective.

King booked $1.9B in 2013 revenue in 2013, with $568M in profit and 665 employees. Supercell (which sold 51% to Softbank for $1.5B in 2013) booked $892M, with $464M EBITDA and 138 employees. Zynga booked $873M in revenue with 2,000 employees, with a $37M loss.

A lot of negativity here, but I think it could be interesting an interesting business. I wouldn't begrudge anyone who has a massive hit like Candy Crush and seeing how far the ride can go.

In my opinion (not investing advice!), they're (investors) exiting now via IPO because their brightest days are behind them. If they're raking in money without millions of shareholders, why would they IPO? They'll paint a rosy picture based on recent performance to pull in several billion dollars, cash out, and move on to the next project. Very, very few game companies make money in the long run ("long" being 5+ years).

Well they've positioned themselves well for the IPO by doing the trademark grab recently. If courts continue to allow them to assert their dominance I think they'll continue to make decent money for a while. I would agree that they're not a long game investment but I think they'll make it over 5 years.

Why not look for someone else to be left holding the bag when the mobile game playing public loses interest in Candy Crush? a la OMGPop/Draw Something selling to Zynga.

I smell a good short. Let's see what level the price is set at and the level of hype in the market. If investors jump on this like it's going to be the next Facebook, there could be a great opportunity here.

I am not a fan of King, but their EBITDA and Net Income are something that many (Valley) gaming companies wished they had. They have some very solid numbers for it to be valued at some random valuation, compared to, for argument sake, Zynga.

I don't think it's a good short because you have no idea if you will have to hold the position for months or a few years before KING drops.

And if it rises too much in the time before your predicted drop then the margin calls will bankrupt you.

As of Q4, the average paying user gave them $17.32 per month in Gross Bookings. And they had $632m of Gross Bookings in the quarter, meaning they had 12.2m paying users by my count, giving them an average of $17.32/mo each.

12.2m paying users out of 408m MAUs, or about 3% of the total.

How does King make its games? Is there a single creative Genius that comes up with everything, like a Sid Meijer or Peter Molyneux kinda person? I would love to know how they operate.

Their games tend to mostly be iterations (or clones if you're cynical) of tries and true successful games that came before and were already proven in the market.

From what I've seen advertised and pop up on facebook etc. Their latest game 'farm heroes saga' screenshots look like 'candy crush saga' but your matching animals instead of candy. I haven't actually played either game so I can't actually state anything in terms of the gameplay.

{kind=link}